TREVISO, Italy – The Board of Directors of De’ Longhi SpA approved on May 12, 2021, the results for the first quarter of 2021¹. Strong growth driven by the coffee machine segment and the increased attention of consumers for the “stay at home”. The company has recently finalized the acquisition Eversys, a Swiss super automatic coffee machine manufacturer.

Key figures for Q1 include:

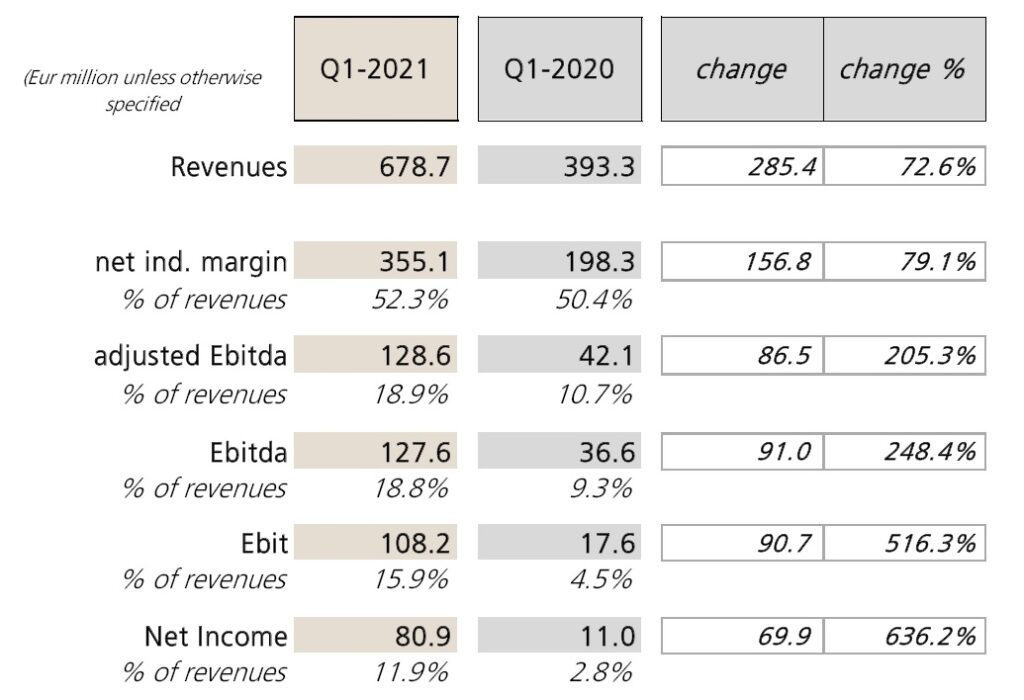

- net revenues of € 678.7 million, up by 72.6%;

- an adjusted² Ebitda of € 128.6 million, up 205.3% and equal to 18.9% of revenues, with an improvement of 8.2 percentage points compared to the previous year;

- Ebit of € 108.2 million, up by 516.3% and equal to 15.9% of revenues;

- a net profit of € 80.9 million, up 636.2%, equal to 11.9% of revenues;

- a positive net financial position of € 318.2 million, improving by € 86.2 million in the quarter.

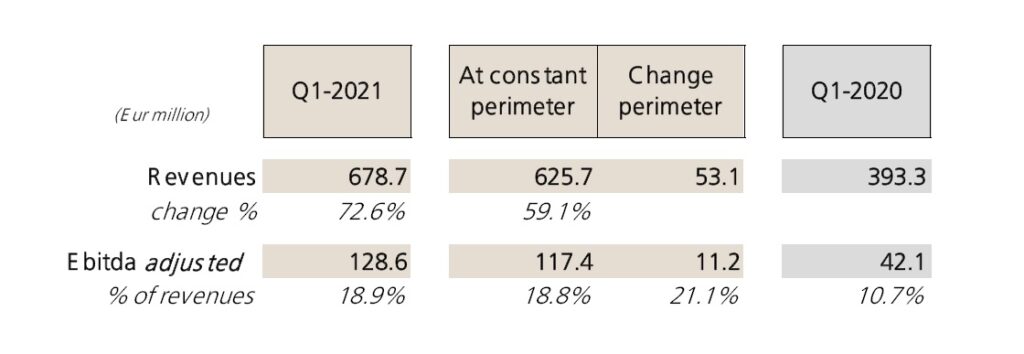

On a like-for-like basis (excluding the newly acquired Capital Brands):

- net revenues of € 625.7 million, up by 59.1% (+ 64.7% at constant exchange rates³);

- an adjusted Ebitda of € 117.4 million, up by 178.8% and equal to 18.8% of revenues.

“The extraordinary results achieved – commented CEO Massimo Garavaglia – further consolidate De’ Longhi’s position among the leaders of the industry. The Group has been able to seize all the opportunities offered by the market in these months of great uncertainty, thanks not only to its brands and products portfolio but also to the great production flexibility and the adaptability of teams and organization. I take this opportunity to thank all the employees of the Group for the dedication, commitment and professionalism shown in recent months, without which we would not have been able to achieve these goals.

Looking at the next future, the continuation of the development trend of coffee and kitchen, strengthened by the increased attention of consumers towards the home environment, support our positive expectations for the coming quarters.

In particular, the signals that we receive from the markets in these first weeks of the second quarter reasonably suggest, for the remaining months of the year, a very robust and more sustained sales trend than initially expected; in light of this, therefore, we revise upwards our guidance for the current year and for the new perimeter including Capital Brands, now forecasting revenues growing at constant exchange rates at a pace between 28% and 33% (i.e. in the range 18 % – 22% on a like-for-like basis) and an adjusted Ebitda in line with 2020 as a percentage of revenues.

This expected dynamic will allow us to continue the previously announced strategy of increasing investments in marketing and communication, in support of our brands and products, thus fueling a virtuous circle aimed at medium-long term growth strategy. ”

¹ The consolidated results of the first quarter of 2021 refer to the new consolidation perimeter of the Group which also includes Capital Brands Holdings Inc. and its subsidiaries, following the acquisition finalized on 29.12.2020.

² “Adjusted” means before non-recurring income / charges and the notional cost of stock option plans.

³ “At constant exchange rates” means excluding the effects of exchange rates’ variations and of hedging derivatives.

Results summary and business review

General Outlook

General Outlook

The first months of 2021 mark a record trend for the Group, both in terms of turnover and margins. The strong growth achieved in this first quarter compares with a first quarter of last year which had shown a growth in sales in the mid-single-digit area, despite initial negative effects of first lockdown.

At the start of the year, consumer demand was the main driver behind the Group’s performance, reinforced by the launches of new products in the last six months and supported by higher spending on communication and marketing activities (so-called “A&P”). These particular conditions have allowed the Group to seize all the opportunities offered by the markets, despite a general climate of persistent uncertainty, thus creating the conditions for a favorable trend in the remainder of the year.

In particular, looking at A&P investments, the Group has launched several activities to support the brands in the long term and to improve consumer engagement, such as the Kenwood Club, the Coffee Lounge and events related to Braun’s 100 year anniversary. During the year, other events will be announced and launched to exploit the potential of our products in the coming quarters.

The Group has also demonstrated, in this quarter as in the full 2020, extraordinary ability to adapt to the new market dynamics, both from a production and organizational point of view. The difficulties created in the supply chain in these months of pandemic have not compromised the operational continuity of the various production platforms of the Group, which have run at full speed in order to satisfy the growing demand from the market.

In the distribution field, the company also reports a significant acceleration of on-line channels, of both those managed by the so-called “pure players” (equal to 20.7% of total sales compared to 19.5% in 2020) and those referring to traditional distribution. In this scenario, direct sales through the proprietary ecommerce platform also increased in weight, reaching 2.1% of sales in the quarter.

Finally, the first quarter of 2021 was the first quarter of full consolidation of Capital Brands Holdings, which contributed to the Group’s results with sales of € 53.1 million and an adjusted Ebitda of € 11.2 million.

Revenues

Revenues

Consolidated revenues for the first quarter amounted to € 678.7 million, growing by 72.6%. The expansion of the Group on a like-for-like basis would have been 59.1% with a turnover of € 625.7 million, up 64.7% at constant exchange rates.

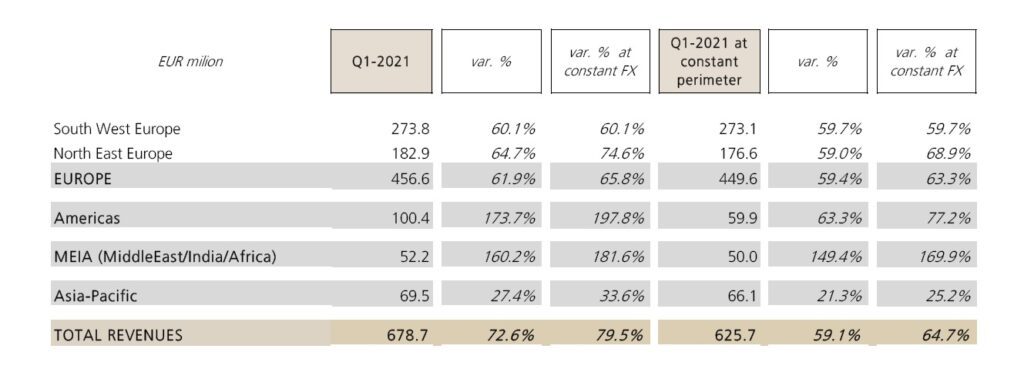

Markets

The start of the year saw all the main geographies in double-digit growth, with a strong recovery compared to the previous year in the MEIA area which grew at a triple-digit rate.

We recall that following the acquisition of Capital Brands Holdings, in the first quarter, North America (USA and Canada) more than doubled its turnover vs. last year and aims to become the Group’s first market on an annual basis.

On a like-for-like basis:

On a like-for-like basis:

- South-West Europe grew by 59.7% with all the main countries accelerating sharply, in particular Italy and France at a rate higher than the Group average;

- North-East Europe also recorded double-digit growth (+ 59%), which showed a particularly robust expansion of Poland and the United Kingdom; a negative currency impact penalized the turnover of the area by approx. 9.9%;

- the Americas area achieved significant growth (+ 63.3%), despite a negative currency impact of approx. 14 percentage points;

- MEIA (Middle East, India, Africa) recovered strongly, with growth at current exchange rates of 149.4%, supported by a significant expansion of all the countries in the region;

- finally, the Asia-Pacific region showed an expansion of + 21.3%, supported in particular by a brilliant trend in coffee and portable heating.

Product segments

During the first quarter of 2021, on a like-for-like basis, almost all of the product segments achieved double-digit growth, supported by the greater investments in communication and marketing envisaged in the plan.

In particular, the world of coffee was favored by an expansion of all the main categories, with a constant exchange rate trend of super-automatic machines above the Group’s average.

The cooking and food preparation segment has benefited from the increased attention of consumers towards products related to the “home experience”, as well as to the themes of healthy food and nutrition. In detail, the kitchen machine segment achieved triple-digit growth in the quarter, while the remaining main sub-categories achieved significant double-digit growth.

As regards the rest of the business, both the cleaning and ironing segment and the comfort segment achieved positive performances, with a significant acceleration in the portable heater category.

Operating margins

As regards the margins evolution in the first three months:

- the net industrial margin, equal to € 355.1 million, improved in terms of percentage of revenues from 50.4% to 52.3% (+ 79.1%), thanks above all to higher volumes and the positive contribution of price-mix;

- adjusted Ebitda amounted to € 128.6 million, equal to 18.9% of revenues; on a like-for-like basis, it stood at € 117.4 million, with a sharp improvement in the margin on revenues from 10.7% to 18.8%;

- Ebitda was € 127.6 million, or 18.8% of revenues; on a like-for-like basis, the margin went from 9.3% of revenues to 18.6%, reaching € 116.4 million;

- Ebit was € 108.2 million, equal to 15.9% of revenues, while on a like-for-like basis it improved from 4.5% to 15.7% of revenues, reaching € 98.1 million;

- finally, net profit was € 80.9 million, equal to 11.9% of revenues (€ 72.7 million, equal to 11.6% of revenues, on a like-for-like basis).

Balance sheet

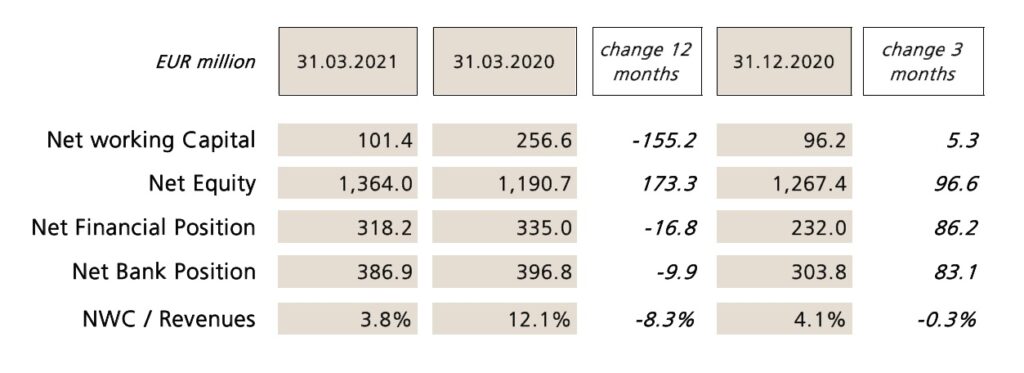

Net financial position as at 31.03.2021 stood at € 318.2 million, with a net cash generation of € 86.2 million in the quarter, after investments for € 19.8 million.

Compared to the same date in 2020, the net financial position decreased by € 16.8 million; however, the free cash flow before dividends and acquisitions was € 393.3 million, thus almost entirely covering both the acquisition of Capital Brands Holdings (€ 329.3 million) and the distribution of dividends for € 80.8 million.

The Group’s net bank position as at 31 March amounted to € 386.9 million, an improvement of € 83.1 million in the quarter.

Net working capital improved significantly compared to last year: the increase in inventories was widely offset in the twelve months by an increase in trade payables, thus bringing the ratio of net working capital to revenues down to 3.8%, a marked reduction compared to last year (12.1%), but in line with the values reached at the end of 2020.

Net working capital improved significantly compared to last year: the increase in inventories was widely offset in the twelve months by an increase in trade payables, thus bringing the ratio of net working capital to revenues down to 3.8%, a marked reduction compared to last year (12.1%), but in line with the values reached at the end of 2020.

The ratio of operating working capital to revenues also improved, decreasing in the 12 months from 14.7% to 9.6%

Events occured after the end of the period

On April 7, the De’ Longhi Group finalized the issue and placement of twenty-year unsecured and non-convertible bonds with US institutional investors (“US Private Placement”) for the amount of Euro 150 million.

On May 3, the acquisition of the entire stake in the Swiss Eversys group, operating in the design and marketing of professional espresso coffee machines, was finalized.