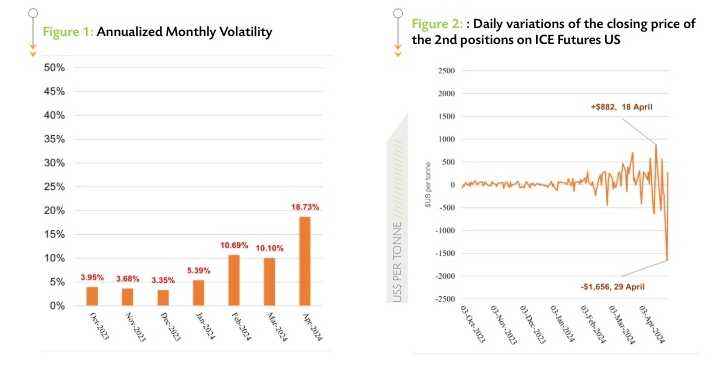

ABIDJAN, Côte d’Ivoire – The extraordinary price rallies recorded in the cocoa futures markets have been accompanied by an increasing volatility. The annualized price volatility of the 2nd position on ICE Futures US moved from about 3.95% in October 2023 to nearly 18.73% in April 2024 (Figure 1).

This made it more expensive and financially risky to maintain a position in the cocoa futures markets (Figure 2). Indeed, the huge daily price variations translated into sizeable margin calls prompting traders to exit the market.

While price volatility has been further amplified by the reduced market liquidity, the most important driver is the great uncertainty about the next crop year. In the absence of reliable statistics on areas under cultivation, tree ages and yields, and the state of spread of Cocoa Swollen Shoot Virus Diseases (CSSVD) in Côte d’Ivoire and Ghana, it is necessary to wait for the completion of pod-counting surveys, expected between the end of August and mid- September, to have an initial estimate of the projected market balance for the 2024/25 year.

Prices are expected to remain high throughout the 2023/24 mid-crop, supported by the current market fundamentals. Indeed, the Conseil du Café-Cacao (CCC) has announced that it expects a 33% year-on-year reduction in the size of the mid-crop from about 400,000 tonnes to 600,000 tonnes.

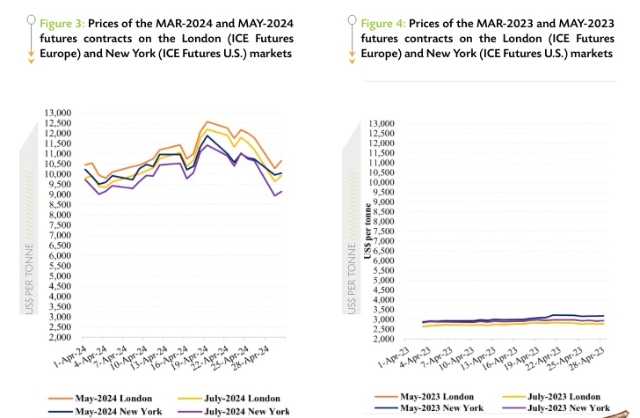

Figure 3 shows price movements of the first and second positions on the London and New York futures markets respectively at the London closing time in April 2024, while Figure 4 presents similar information for the previous year.

Over the month under review, prices of the front-month contract averaged US$11,042 per tonne and ranged between US$9,800 and US$12,567 per tonne in London while in New York, they averaged US$10,446 per tonne and fluctuated between US$9,500 and US$11,878 per tonne. Compared to the average prices recorded a year ago (US$2,752 per tonne in London and US$3,040 per tonne in New York), the average prices seen in April 2024 represented significant increases of 301% and 244% respectively.

After the nearby May-24 contract attained an all-time high on 19 April 2024 of US$12,567 per tonne in London and US$11,878 per tonne in New York, cocoa futures by the end of the month declined by 15% on both markets to US$10,662 per tonne and US$10,050 per tonne in London and New York, respectively.

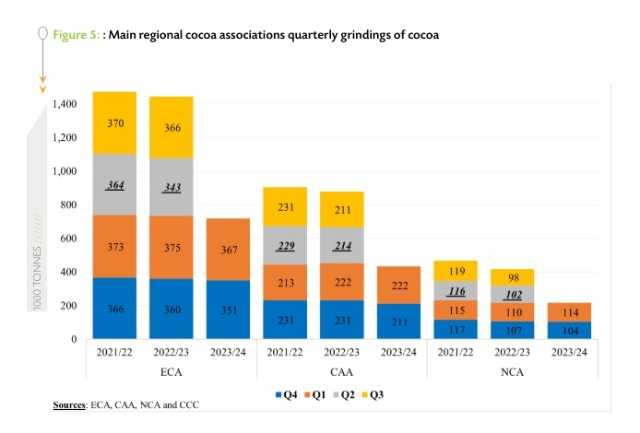

Grindings data published by regional associations for Q1.2024 depict that demand does not seem to neutralize the deficit. Whereas Europe’s Q1.2024 cocoa grindings as reported by the European Cocoa Association (ECA) fell by 2.2% from a year earlier to 367,287 tonnes, that of North America published by the National Confectioners Association (NCA) rose by 3.6% year-on-year to 113,683 tonnes.

Data from the Cocoa Association of Asia (CAA) revealed a slight drop of 0.2% year-on-year to 221,530 tonnes (Figure 5).

Some analysts are of the view that the increase in North American grindings may be due to panic buying in the chocolate industry as chocolate makers are buying as much as they can before a shortage in supplies occurs . Also due to the forward contracting strategy, manufacturers may currently be covered, and processing may not see an immediate significant decline for the rest of the season.