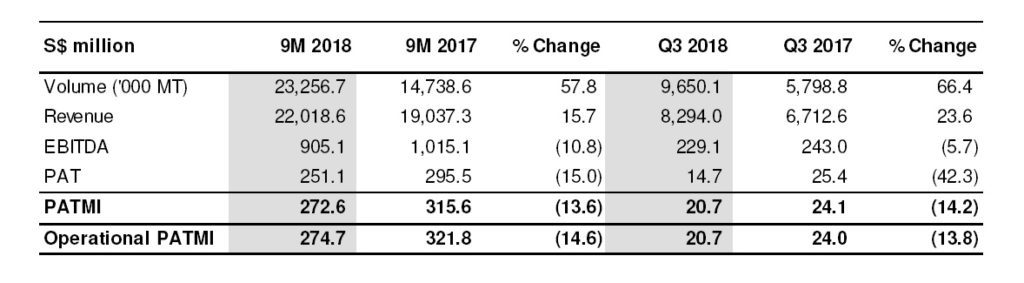

SINGAPORE – Olam International Q3 profits drop 14.2% to $20.7m from $24.11m in 2017, the company reported on Wednesday. However, its revenue jumped 23.6% to $8.29m from $6.71m.

The decline in profits was primarily caused by tough trading conditions in coffee and lower contribution form the peanut business and commodity financial services (CFS), according to its financial statement.

Operational profit after tax and minority interests also fell 13.8% to $20.7m from $24m in 2017, the firm noted.

Olam International saw its profits fall 36.4% YoY to $93.91m in Q2 on the back of weak sales from coffee, peanuts and edible oils segment.

Co-Founder & Group CEO, Sunny Verghese said:

“Our Q3 is a seasonally lower quarter which was further impacted by ongoing tough trading conditions in Coffee, lower performance from the peanut business and the Commodity Financial Services business.

“We further refined our portfolio and made targeted investments during the year, including into digital initiatives and sustainability solutions, that will position us to capture future growth.”

Executive Director and Group COO, A. Shekhar said:

“Our proactive efforts to strengthen our financial position and capital structure have supported our performance. We reduced our gearing and overall net debt with lower finance costs despite higher interest rates, while continuing to diversify our funding sources. Our focus on capital productivity has resulted in delivering S$602.4 million in Free Cash Flow to Equity for 9M 2018.”

Financial Results

Q3 2018

– PATMI (Profit After Tax and Minority Interest) down 14.2% year-on-year (YoY) to S$20.7 million (Q3 2017: S$24.1 million) against a strong Q3 2017, mainly due to lower contribution from Coffee, Peanuts and CFS.

– Operational PATMI, which excludes exceptional items, declined 13.8% YoY to S$20.7 million (Q3 2017: S$24.0 million).

– EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) was down 5.7% at S$229.1 million (Q3 2017: S$243.0 million).

9M 2018

– PATMI declined 13.6% YoY to S$272.6 million (9M 2017: S$315.6 million) against a strong 9M 2017, mainly due to the tough trading conditions in Coffee and lower contribution from Peanuts and CFS.

– Operational PATMI was lower by 14.6% YoY at S$274.7 million (9M 2017: S$321.8 million).

– EBITDA was down 10.8% at S$905.1 million (9M 2017: S$1.0 billion).

Cash flow and gearing

– Net gearing as at September 30, 2018 was significantly lower at 1.38 times (September 30, 2017: 1.82 times), as net debt came down by S$1.3 billion with the reduction in working capital, lower gross capital expenditure, cash from divestments and the conversion of warrants into equity.

– FCFE for Q3 2018 improved to S$769.4 million (Q3 2017: S$726.0 million) while FCFE for 9M 2018 was S$602.4 million versus S$713.2 million in the prior period.

9M 2018 Segmental Performance

Edible Nuts, Spices & Vegetable Ingredients (SVI)

– Revenue declined by 4.2% to S$3.2 billion due to lower peanut sales.

– EBITDA fell by 18.3% to S$277.0 million, when compared with strong performance in 9M 2017. The results in 9M 2018 were impacted by the peanut businesses in Argentina and the US, which offset the improved performance by SVI, excluding tomato processing.

Confectionery & Beverage Ingredients

– Revenue decreased 15.4% to S$5.2 billion on lower volumes and lower coffee prices.

– EBITDA improved 12.1% to S$278.9 million as strong performance in the Cocoa supply chain and processing compensated for weaker results from Coffee, which continued to face difficult market conditions.

Food Staples & Packaged Foods

– Revenue was up 60.9% to S$10.2 billion on significant volume growth driven by higher Grains trading volumes.

– EBITDA declined 14.6% to S$248.7 million against a very strong 9M 2017 on lower contribution from Edible Oils, Sugar and Dairy, which offset the improved results from Grains and Packaged Foods.

Industrial Raw Materials, Ag Logistics & Infrastructure

– Revenue grew 6.0% to S$3.4 billion on higher Wood Products sales and prices in the Republic of Congo with improved demand from European markets.

– EBITDA fell 4.8% to S$132.4 million on relatively lower contribution from Cotton, which offset growth from GSEZ, Wood Products and Rubber.

Commodity Financial Services

– CFS reported higher EBITDA losses of S$31.9 million (9M 2017: -S$3.1 million) mainly due to losses from the Funds business.

Outlook

While global markets are experiencing heightened political and economic uncertainties, Olam believes its diversified and well-balanced portfolio provides a resilient platform to navigate the challenges in both the global economy and commodity markets.

Olam will continue to execute on its 2016-2018 Strategic Plan for the rest of 2018 and focus on growing its prioritised platforms, turning around underperforming businesses, ensuring gestating businesses reach full potential and delivering positive free cash flow.