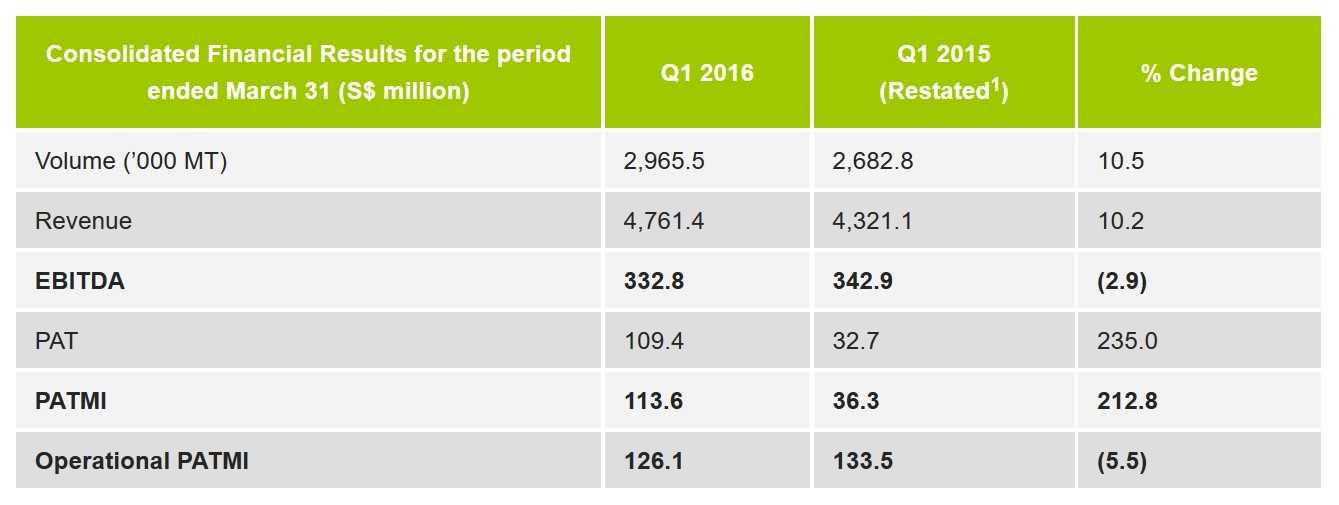

Olam International Limited has reported improved year-on-year earnings for the quarter ended March 31, 2016 (Q1 2016). Profit After Tax and Minority Interest (PATMI) increased 212.8% to S$113.6 million, from S$36.3 million in the previous corresponding period.

This was primarily due to lower exceptional charges, resulting from the buy-back of high priced bonds in both periods (Q1 2016: S$12.5 million; Q1 2015: S$97.2 million).

Operational PATMI, which excludes exceptional items, declined by 5.5% to S$126.1 million as the Group’s Earnings Before Interest, Tax, Depreciation, and Amortisation (EBITDA) edged down 2.9% to S$332.8 million.

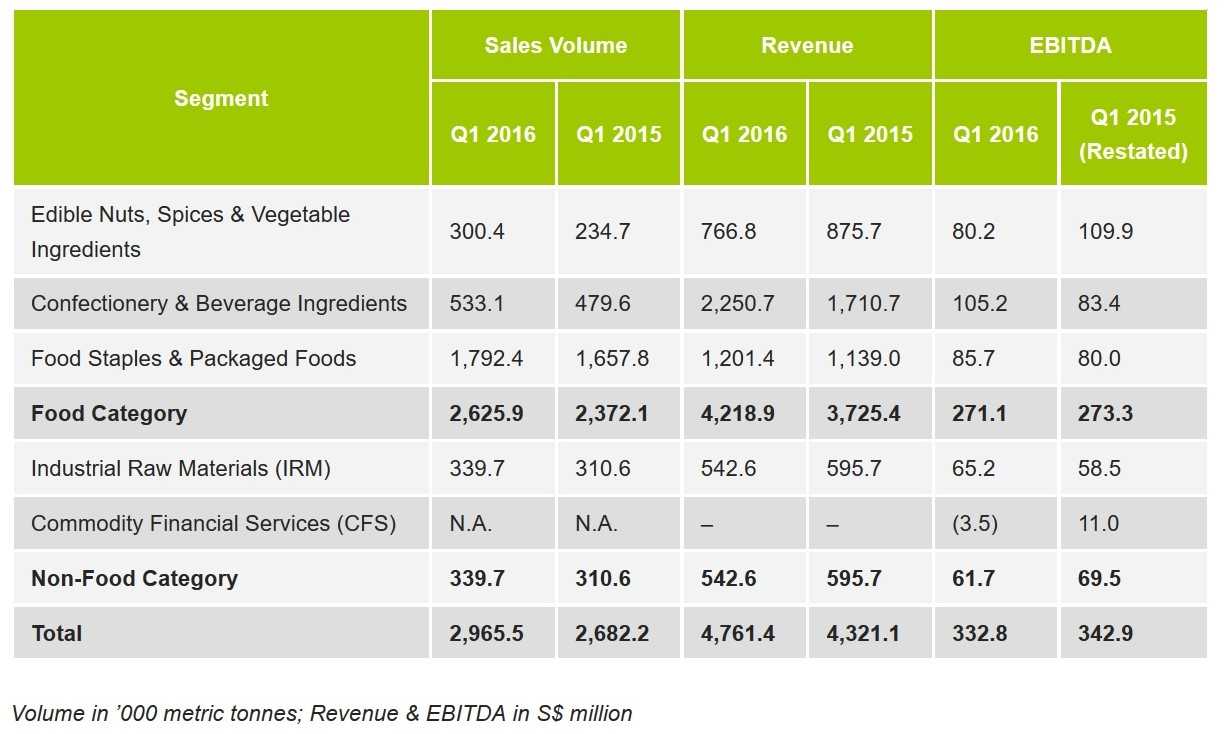

EBITDA growth in the Confectionery & Beverage Ingredients, Food Staples & Packaged Foods and Industrial Raw Materials segments was offset by lower contribution from the Edible Nuts, Spices & Vegetable Ingredients and Commodity Financial Services segments.

Sales volumes and revenues in Q1 2016 were up 10.5% and 10.2% respectively, as all business segments posted higher volumes.

As a result of various initiatives to optimise debt tenure and reduce cost of borrowing, Olam recorded lower net finance costs of S$99.4 million, a 19.3% improvement from a year ago, despite growth in invested capital.

Olam recorded higher depreciation and amortisation of S$80.5 million, compared to S$58.3 million in Q1 2015, due to a higher asset base resulting from the acquisition of ADM’s cocoa processing business (Cocoa Processing assets) and the wheat milling and pasta manufacturing assets of the BUA Group in Nigeria.

The results also included a net loss of S$5.3 million on the fair valuation of biological assets compared to a net loss of S$1.9 million in Q1 2015.

Both net change in fair value of biological assets and depreciation and amortisation are reported in accordance with the amendments to Singapore Financial Reporting Standards (SFRS) 16 (Property, Plant and Equipment) and SFRS 41 (Agriculture), which took effect on January 1, 2016.

The Group generated positive net operating cash flow of S$309.9 million during the period (Q1 2015: S$209.4 million). However, Olam reported a negative Free Cash Flow to Firm of S$156.0 million primarily due to the acquisition of the wheat milling and pasta manufacturing assets in Nigeria (S$311.7 million).

Net gearing stood at 1.97 times as at March 31, 2016, up marginally from 1.96 times as at end-December 2015 and within the Group’s strategic plan target of 2.0 times or lower.

Post Q1 2016, Olam announced two major business initiatives. In April, it announced a 30:70 joint venture in Japan with its strategic partner Mitsubishi Corporation.

The new entity, MC Agri Alliance Ltd, will import and distribute coffee, cocoa, sesame, edible nuts, spices, vegetable ingredients and tomato products for the Japanese market.

The Company also announced its plans to invest US$150.0 million to set up two state-of-the-art animal feed mills, poultry breeding farms and a hatchery in Nigeria.

Olam’s Co-Founder & Group CEO Sunny Verghese said: “Our consistent performance amid challenging market conditions and uneven global growth reflects our sound business fundamentals and our diversified portfolio.

“We are confident about our growth prospects, on the back of our acquisition of ADM’s cocoa processing assets, BUA Group’s wheat milling assets, our entry into the animal feed business in Nigeria and our new joint venture with Mitsubishi Corporation in Japan. These initiatives will open up new opportunities and revenue streams as we continue to execute on our differentiated strategy.”

Segmental Review

Olam’s Executive Director and Group COO, A. Shekhar said: “We are pleased to report that most of our business segments delivered resilient EBITDA growth despite the macroeconomic uncertainty and high volatility that we are experiencing across most capital and commodity markets globally. Our debt optimisation programme has lowered our costs of borrowing and we remain focused on delivering profitable growth.”

The Edible Nuts, Spices & Vegetable Ingredients segment registered a 28.0% year-on- year volume increase on higher volumes for nearly all products within the segment, especially for the peanut business post the full consolidation of the results of McCleskey Mills for the quarter.

However, revenues declined 12.4% as prices fell across most products. EBITDA fell 27.0% as declining almond prices and lower market prices and margins for tomato processing offset enhanced contribution from cashew, sesame, spices and vegetable ingredients during the quarter.

The Confectionery & Beverage Ingredients segment recorded an 11.2% increase in volumes for Q1 2016, mainly from the consolidation of results from the Cocoa Processing assets. Revenues grew 31.6% on the higher volumes as well as higher cocoa prices. EBITDA grew 26.2% with increased contribution from the Cocoa Processing assets and improved performance from the Coffee platform.

Food Staples & Packaged Foods segment recorded an 8.1% year-on-year volume increase driven by the West Africa wheat milling business and steady growth in the Dairy, Rice, Palm and Sugar supply chain businesses. As a result of higher volumes, revenue increased by 5.5% despite lower prices for most commodities within the segment.

EBITDA increased by 7.1% with improved performance across most of the platforms. The Dairy, Rice and Palm supply chain businesses, wheat milling operations in Africa and Dairy farming operations in Russia showed growth in their overall EBITDA, whilst Packaged Foods and Sugar were flat.

Dairy farming in Uruguay saw improved operational performance and lower costs although some of these gains were offset by the negative impact from lower milk prices.

The Industrial Raw Materials segment recorded a 9.4% growth in volumes as all products reported higher volumes. However, revenues declined by 8.9% as lower prices across all commodities within this segment offset the higher volumes. Despite lower revenue, EBITDA improved by 11.5% based on the performance of Cotton and Wood Products businesses.

Commodity Financial Services booked an EBITDA loss of S$3.5 million in Q1 2016 compared to a positive EBITDA of S$11.0 million in Q1 2015.

Outlook and Prospects

The long-term trends in the agri-commodity sector remain attractive, and Olam is well positioned to benefit from this as a core global supply chain business with selective integration into higher value upstream and mid/downstream segments. Olam believes its diversified and well-balanced portfolio with leadership positions in many segments provides a resilient platform to navigate current uncertainties in global markets.

1 Prior period financial statements have been restated due to changes in accounting standards relating to SFRS 16 and SFRS 41 that were effective from January 1, 2016. Please refer to the notes to editors and pages 5-8 of the Management Discussion and Analysis report for more information.