MILAN – The United States Department of Agriculture (Usda) released on Friday its biannual report “Coffee: World Markets and Trade” containing the official estimates on production and consumption. World coffee production for 2019/20 is forecast 5.3 million bags (60 kilograms) lower than the previous year to 169.3 million, primarily due to Brazil’s Arabica trees entering the off-year of the biennial production cycle.

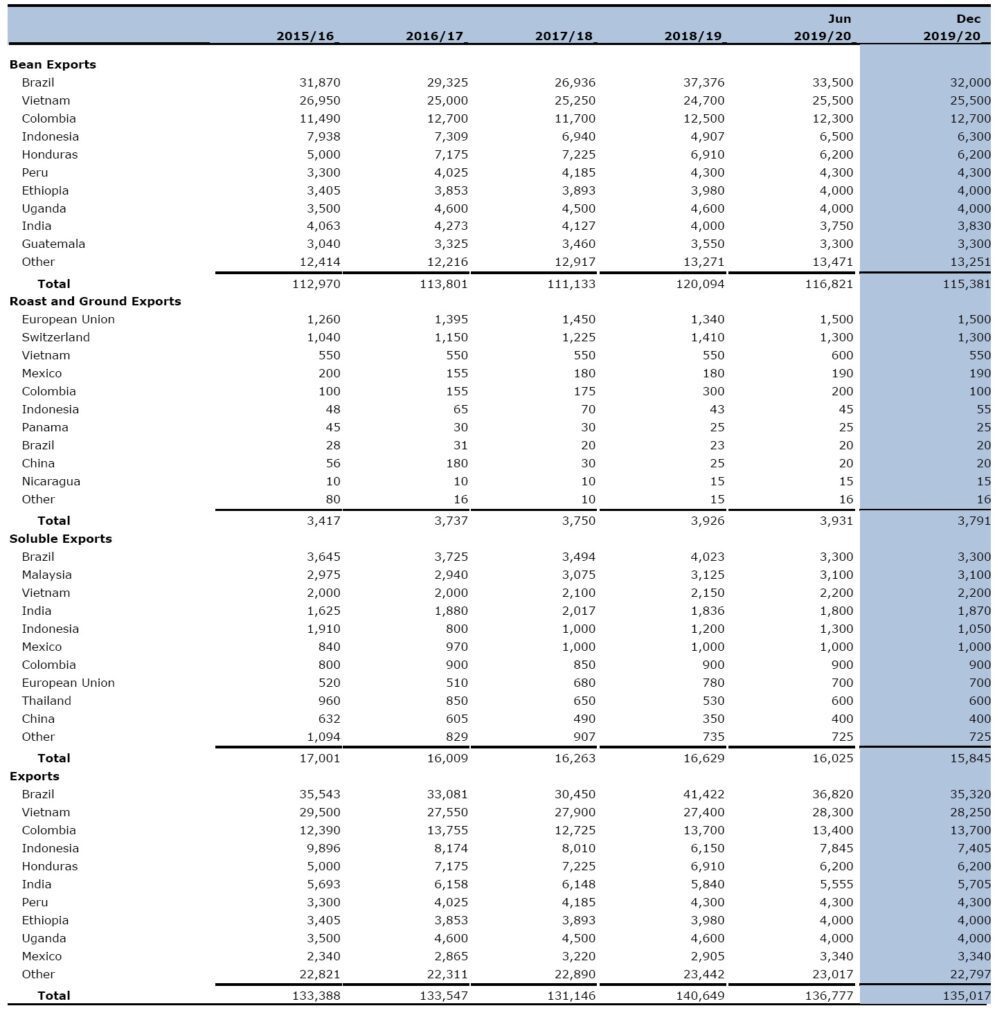

World exports are expected down 4.7 million bags to 115.4 million primarily due to lower shipments from Brazil and Honduras.

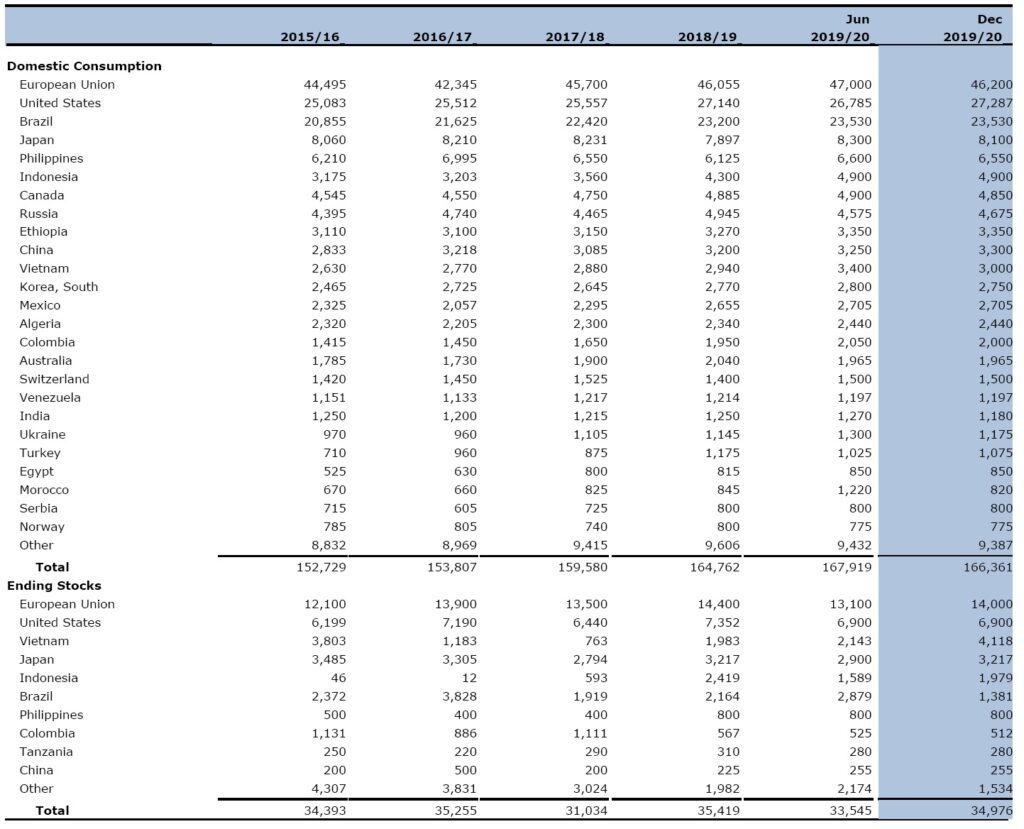

With global consumption forecast at a record 166.4 million bags, ending inventories are expected to slip 400,000 bags to 35.0 million.

Coffee prices, as measured by the International Coffee Organization (ICO) monthly composite price index, dropped to $0.93 per pound in May 2019, the lowest since September 2006, but rebounded 15 percent to $1.07 by November 2019 as supplies tighten. http://www.ico.org/new_historical.asp

Brazil’s Arabica output is forecast to drop 8.3 million bags to 39.9 million compared to the previous season since most trees are in the off-year of the biennial production cycle. Good weather conditions generally prevailed in most coffee growing regions during the blossoming and fruit-forming stages.

Despite initial concerns related to July frost in southern and southeastern states, yields were not adversely impacted by this weather event. However, coffee quality as well as bean size were lower than average, because trees in many areas had multiple stages of maturity when the coffee cherries were harvested.

The bulk of the Arabica harvest started in May and June. The Robusta harvest is forecast to continue expanding and to reach a record 18.1 million bags, up 1.5 million. Abundant rainfall aided fruit development in the major producing state of Espirito Santo, while good crop management practices supported a steady increase in the state of Rondonia. Most of the Robusta harvest started in April and May.

However, the combined Arabica and Robusta harvest is forecast down 6.8 million bags to 58.0 million. With reduced supplies, bean exports are expected to drop 5.4 million bags to 32.0 million and ending stocks are forecast to decline 800,000 bags to 1.4 million. Consumption is expected to continue rising to a record 23.5 million bags.

Vietnam’s coffee production is forecast at a record 32.2 million bags, up 1.8 million from the previous year due to continued expansion of area planted as well as favorable weather that boosted yields. Between January and early April 2019, the main coffee regions in the Central Highlands experienced seasonally dry and sunny weather, and trees were irrigated.

The rainy season was slightly delayed, but adequate during July and August to support good flowering and fruit-set. With black pepper prices falling over the last 3 years, farmers are no longer replacing coffee trees with pepper.

However, some farmers have begun to plant durian, mango, avocado, and passion fruit trees in their coffee orchards. Bean exports are forecast 800,000 bags higher to 25.5 million, while ending stocks are seen more than doubling to 4.1 million bags as recent prices provide less incentive to sell.

Total coffee production for Central America and Mexico is forecast down slightly by 400,000 bags to 19.1 million as some countries in the region struggle to rebound from the coffee rust outbreak that first lowered output in 2013/14.

Gains in Mexico on favorable weather are expected to offset losses in Honduras, where farmers have reduced preventative measures to combat coffee rust due to low prices and limited ability to extend existing loans. El Salvador, and Panama are flat at 650,000 bags and 75,000 bags, respectively, as these countries continue to struggle with rust and output remains below their pre-rust level.

Nicaragua is forecast 300,000 bags lower to 2.3 million as financial constraints are expected to lead to reduced inputs and yields. Guatemala is expected 200,000 bags lower to 3.6 million on reduced yields. Bean exports for the region are forecast to lose 800,000 bags to 15.5 million mainly due to lower exportable supplies in Honduras.

Nearly half of the region’s exports are destined for the European Union, followed by about one-third to the United States.

Colombia’s production is forecast to rebound 400,000 bags from last year’s drought-related shortfall to reach 14.3 million on normal growing conditions.

The National Federation of Coffee Growers of Colombia (FEDECAFE) estimates that since 2012, about half of the 940,000 hectares of coffee have been renovated, mostly with rust-resistant varieties. This effort has boosted yields nearly one-third to 18.8 bags per hectare and has lowered the average age of coffee trees from 15 to 7 years.

FEDECAFE and the Colombian government renovated an estimate 82,000 hectares in 2018, with the goal of renovating 90,000 hectares annually to reach the production goal of 18 million bags in the coming years. Bean exports are seen up 200,000 bags to 12.7 million, while ending stocks are expected to dip slightly to 500,000 bags.

Indonesia’s production is forecast to gain a modest 100,000 bags to 10.7 million, with the gain split evenly between Arabica and Robusta output. Robusta production is expected to reach 9.5 million bags on favorable growing conditions in the lowland areas of Southern Sumatra and Java, where approximately 75 percent is grown. Despite heavy rainfall in West Java that delayed its Arabica harvest, output is expected up slightly.

Although recent news reports suggest total output may jump significantly over the next 5 years, these claims have not been supported by a noticeable increase in planted area or by a renovation program to replace older trees with higher-yielding varieties, and fertilizer utilization has remained largely unchanged. Bean exports are forecast to rebound 1.4 million bags to 6.3 million, boosted by last year’s elevated ending stocks.

EU imports are forecast down 1.1 million bags to 48.0 million and account for over 40 percent of the world’s coffee bean imports. Top suppliers include Brazil (29 percent), Vietnam (25 percent), Honduras (8 percent), and Colombia (6 percent). Ending stocks are expected down 400,000 bags to 14.0 million.

The United States imports the second-largest amount of coffee beans and is forecast 1.0 million bags lower to 26.2 million. Top suppliers include Brazil (24 percent), Colombia (22 percent), Vietnam (15 percent), and Guatemala (6 percent). Ending stocks are forecast 500,000 bags lower to 6.9 million but consumption is little changed following last year’s gain.

Revised 2018/19

World coffee production is 174.6 million bags, nearly unchanged from the June 2019 estimate.

World bean exports are raised 2.5 million bags to 120.1 million.

- Brazil is up 1.4 million bags to 37.4 million on higher-than-anticipated stocks drawdown.

- Cote d’Ivoire is raised 300,000 bags to 1.7 million on greater exportable supplies.

World bean imports are raised 2.0 million bags to 115.7 million.

- The United States is up 1.1 million bags to 27.2 million on higher consumption and stocks.

- Colombia is revised 400,000 bags higher to 1.1 million on stronger shipments from Peru and Honduras.

World ending stocks are reduced 900,000 bags to 35.4 million.

- Brazil is lowered 1.7 million bags to 2.2 million on higher shipments to the European Union and the United States.

- European Union is raised 600,000 bags to 14.4 million.

- The United States is up 700,000 bags to 7.4 million.